This post is about the story of ‘Alpha’. In the world of investing and trading, we all use the word ‘alpha’ a lot. But where does it come from, and what does it mean?

Let’s start with what is Alpha.

Alpha refers to the excess returns a security generates compared to a benchmark e.g. an Index.

Say you create a portfolio that generated 15% returns in the last FY, and the index did 5% in the same period. You can say you generated a 10% alpha

But actually, just comparing returns doesn’t give you a full picture. You need to compare risk as well. Hang on that’ll get covered by the end.

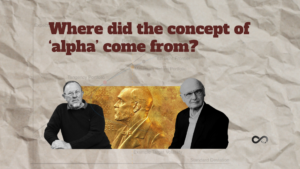

Here’s how it all started.

In mid-1950’s a young economics graduate Harry Markowitz was working on the concept of a mean-variance portfolio. It’s a portfolio where the expected return is maximized for a given level of risk.

But he encountered a problem – what does he compare the returns and risk of this portfolio to?

This is where another researcher William Sharpe happens to join the Rand Corporation, and was looking for a research topic. Markowitz suggests working on Portfolio theory.

They found a solution, i.e. to create what was then known as a ‘market portfolio’ and what we call today the market-cap-weighted portfolio came into existence. With S&P 500 being the first to adopt it in the year 1957.

Sharpe moved to solve the next question. Among all the stocks, should a given stock be included in a portfolio? To answer that question, he came up with the Capital Asset Pricing Model popularly known as CAPM.

Essentially CAPM is a formula that takes the following inputs and gives (α) as the output

Inputs -> market returns; stock returns; risk-free rate; beta of the stock

Output -> alpha; +ve alpha means the stock has done better than the index

Now you may ask what is this Beta?

Beta is a measure of the relative risk compared to the market index.

A beta of 1.2 means the stock will move 1.2 times the move of the market. So, in short Alpha is about relative return, and Beta is about relative risk.

The CAPM model is where the word ‘Alpha‘ comes from.

So the next time you use the word ‘Alpha’ do remember to thank Markowitz and Sharpe. They were the ones to invent it, and yes, they even went on to win the Nobel Prize.

While this thread was more about the concept of Alpha, but you may ask where does alpha come from? Why do some strategies outperform others? But that’s for another post.